Investor ResourcesCountriesTanzania

Navigate this page

Overview

60 Million+ (90.2%)

Clean cooking population without access (World Bank, 2023)

25+

Active clean cooking ventures (Source: CCA)

4+

Number of clean cooking RBFs (Source: CCA)

Click “Read More” for a detailed overview

Tanzania’s clean cooking sector is undergoing a significant transformation aimed at addressing health, environmental, and economic challenges associated with traditional cooking methods.

As of recent assessments, a vast majority of Tanzanian households rely on biomass fuels for cooking, with approximately 84.8% of rural households and 17.4% of urban households using firewood(Eni). Annually, around 469,420 hectares of forests are destroyed for firewood and charcoal production(Eni).

To combat this, the Government of Tanzania has launched the National Clean Cooking Strategy (NCCS) 2024-2034, targeting an 80% adoption rate of clean cooking solutions by 2034 (Tanzania Ministry of Energy).

Supply

Demand

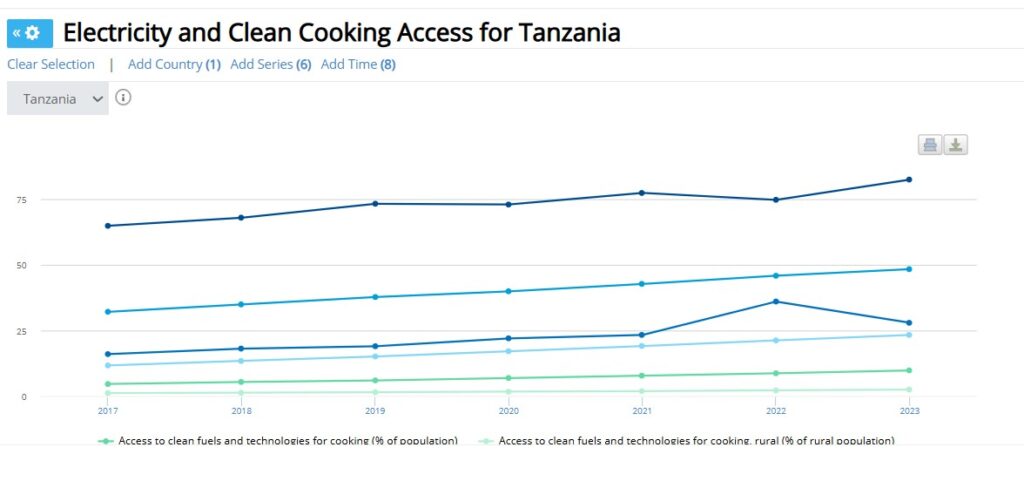

According to World Bank data, 9.8% of the population had access to clean fuels and technologies for cooking in 2023, which rose from 8.7% in 2022. In 2023, 23.3% of the urban population had access to clean cooking fuels, compared with just 2.5% of the rural population.

Access to electricity in Tanzania is relatively higher: 48.3% of the population had access in 2023, up from 45.8% in 2022.

While there has been progress in increasing access to electricity, particularly in urban areas, the adoption of clean cooking fuels and technologies remain low, especially in rural regions. These figures underscore the ongoing challenges and efforts in improving energy access in Tanzania, highlighting the need for continued investment and policy focus, particularly in rural areas

Policy

Click ‘Read more’ to explore relevant aspects of Tanzania’s Nationally Determined Contribution and other policies relevant to clean cooking.

Nationally Determined Contributions

Tanzania’s updated Nationally Determined Contribution (NDC), submitted in 2021, places a strong emphasis on clean cooking as a key strategy for both climate change mitigation and sustainable development. The country has committed to reducing its greenhouse gas emissions by 30–35% by 2030 relative to a business-as-usual scenario. A significant portion of this reduction is expected to come from the energy and forestry sectors, where the widespread use of biomass for cooking is a major source of emissions and deforestation. Transitioning to clean cooking technologies is therefore seen as essential to achieving Tanzania’s climate targets.

In the energy sector, the NDC outlines plans to scale up the adoption of clean cooking solutions, including liquefied petroleum gas (LPG), improved biomass stoves, biogas, ethanol, and electric cooking. These technologies offer a pathway to reduce household reliance on woodfuel and charcoal, both of which contribute to indoor air pollution and forest degradation. The NDC further acknowledges that tackling these issues will require supportive policies, public-private partnerships, and accessible financing mechanisms to ensure that clean cooking options are both affordable and widely adopted.

Beyond emissions reduction, clean cooking is positioned in the NDC as a solution with significant co-benefits. From a public health perspective, reducing exposure to household air pollution will lower the incidence of respiratory diseases and premature deaths, particularly among women and children. The transition also has gender and social equity implications, as it relieves women and girls of the time and physical burden associated with collecting firewood—opening up opportunities for education and income generation. In rural communities, improved access to clean cooking enhances resilience by reducing dependence on increasingly scarce biomass resources.

The importance of clean cooking has also been reinforced by the government’s launch of the National Strategy for Clean Cooking Energy (2024–2034), which aims to increase clean cooking access from the current 10% to 80% by 2034. This strategy supports the implementation of the NDC through actions such as fiscal incentives for clean cooking technologies and the enforcement of standards for institutional cooking in schools and hospitals.

However, Tanzania’s ability to realize these clean cooking ambitions is heavily dependent on international support. The NDC highlights the need for financial resources, technology transfer, and capacity building to accelerate progress. In this way, clean cooking is not only a mitigation priority—it is a cross-cutting development strategy that aligns with national goals for health, gender equality, environmental sustainability, and energy access.

| Source | Tanzania NDCs-2021 |

Tax and Tariff Data

This table shows Tanzanian duty and VAT levels for clean cooking items:

| RTAs | Official designation | HS Code | Tax or tariff | Quantity | Notes |

| EAC, COMESA | Electricity | HS 2716 | MFN import duty | 0% | Electricity may be imported duty free |

| EAC, COMESA | Electricity | HS 2716 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Electricity | HS 2716 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Electricity | HS 2716 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Undenatured ethyl alcohol of an alcoholic strength by volume of 80 % vol or higher | HS 2207.10 | MFN import duty | 35% | Any supplies for diagnosis, prevention, treatment, and management of epidemics, pandemics and health hazards as recommended by the competent authority in the Ministry responsible for Health are duty free. |

| EAC, COMESA | Undenatured ethyl alcohol of an alcoholic strength by volume of 80 % vol or higher | HS 2207.10 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Undenatured ethyl alcohol of an alcoholic strength by volume of 80 % vol or higher | HS 2207.10 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Undenatured ethyl alcohol of an alcoholic strength by volume of 80 % vol or higher | HS 2207.10 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Ethyl alcohol and other spirits, denatured, of any strength | HS 2207.20 | MFN import duty | 35% | Any supplies for diagnosis, prevention, treatment, and management of epidemics, pandemics and health hazards as recommended by the competent authority in the Ministry responsible for Health are duty free. |

| EAC, COMESA | Ethyl alcohol and other spirits, denatured, of any strength | HS 2207.20 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Ethyl alcohol and other spirits, denatured, of any strength | HS 2207.20 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Ethyl alcohol and other spirits, denatured, of any strength | HS 2207.20 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Illuminating kerosene | HS 2710.19.22 | MFN import duty | 0% | Illuminating kerosene may be imported duty free |

| EAC, COMESA | Illuminating kerosene | HS 2710.19.22 | VAT | 0% | Goods falling under this subheading are exempted from value added tax. |

| EAC, COMESA | Illuminating kerosene | HS 2710.19.22 | Other taxes and tariffs | 465 TZS/l | Excise duty is levied at a rate of 465 TZS/l. |

| EAC, COMESA | Illuminating kerosene | HS 2710.19.22 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Illuminating kerosene | HS 2710.19.22 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Propane | HS 2711.12 | MFN import duty | 0% | Propane may be imported duty free |

| EAC, COMESA | Propane | HS 2711.12 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Propane | HS 2711.12 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Propane | HS 2711.12 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Butane | HS 2711.13 | MFN import duty | 0% | Butane may be imported duty free |

| EAC, COMESA | Butane | HS 2711.13 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Butane | HS 2711.13 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Butane | HS 2711.13 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Petroleum gases and other gaseous hydrocarbons — Liquefied — Other | HS 2711.19 | MFN import duty | 0% | LPG may be imported duty free |

| EAC, COMESA | Petroleum gases and other gaseous hydrocarbons — Liquefied — Other | HS 2711.19 | VAT | 0% | Value added tax is applied at a rate of 18% of the duty paid value. Liquid petroleum gas is exempted from value added tax. |

| EAC, COMESA | Petroleum gases and other gaseous hydrocarbons — Liquefied — Other | HS 2711.19 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Petroleum gases and other gaseous hydrocarbons — Liquefied — Other | HS 2711.19 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Fuelwood – Non-coniferous | HS 4401.12 | MFN import duty | 0% | Fuelwood may be imported duty free |

| EAC, COMESA | Fuelwood – Non-coniferous | HS 4401.12 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Fuelwood – Non-coniferous | HS 4401.12 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Fuelwood – Non-coniferous | HS 4401.12 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Wood pellets | HS 4401.31 | MFN import duty | 0% | Wood pellets may be imported duty free |

| EAC, COMESA | Wood pellets | HS 4401.31 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Wood pellets | HS 4401.31 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Wood pellets | HS 4401.31 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Wood briquettes | HS 4401.32 | MFN import duty | 0% | Wood briquettes may be imported duty free |

| EAC, COMESA | Wood briquettes | HS 4401.32 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Wood briquettes | HS 4401.32 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Wood briquettes | HS 4401.32 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Sawdust and wood waste and scrap, agglomerated in logs, briquettes, pellets or similar forms – other | HS 4401.39 | MFN import duty | 0% | Wood waste briquettes may be imported duty free |

| EAC, COMESA | Sawdust and wood waste and scrap, agglomerated in logs, briquettes, pellets or similar forms – other | HS 4401.39 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Sawdust and wood waste and scrap, agglomerated in logs, briquettes, pellets or similar forms – other | HS 4401.39 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Sawdust and wood waste and scrap, agglomerated in logs, briquettes, pellets or similar forms – other | HS 4401.39 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Charcoal, other wood | HS 4402.90 | MFN import duty | 0% | Wood charcoal may be imported duty free |

| EAC, COMESA | Charcoal, other wood | HS 4402.90 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Charcoal, other wood | HS 4402.90 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Charcoal, other wood | HS 4402.90 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Charcoal, of bamboo | HS 4402.10 | MFN import duty | 0% | Bamboo charcoal may be imported duty free |

| EAC, COMESA | Charcoal, of bamboo | HS 4402.10 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Charcoal, of bamboo | HS 4402.10 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Charcoal, of bamboo | HS 4402.10 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Charcoal, of shell or nut | HS 4402.20 | MFN import duty | 0% | Shell or nut charcoal may be imported duty free |

| EAC, COMESA | Charcoal, of shell or nut | HS 4402.20 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Charcoal, of shell or nut | HS 4402.20 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Charcoal, of shell or nut | HS 4402.20 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Cooking appliances and plate warmers, for gas fuel or gas + other fuels | HS 7321.11 | MFN import duty | 10% | |

| EAC, COMESA | Cooking appliances and plate warmers, for gas fuel or gas + other fuels — Presented completely knocked down (CKD) or unassembled for the assembly industry. | HS 7321.11 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Cooking appliances and plate warmers, for gas fuel or gas + other fuels — Presented completely knocked down (CKD) or unassembled for the assembly industry. | HS 7321.11 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Cooking appliances and plate warmers, for gas fuel or gas + other fuels — Presented completely knocked down (CKD) or unassembled for the assembly industry. | HS 7321.11 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Cooking appliances and plate warmers, for liquid fuels | HS 7321.12 | MFN import duty | 25% | |

| EAC, COMESA | Cooking appliances and plate warmers, for liquid fuels | HS 7321.12 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Cooking appliances and plate warmers, for liquid fuels | HS 7321.12 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Cooking appliances and plate warmers, for liquid fuels | HS 7321.12 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Cooking appliances and plate warmers, including for solid fuels | HS 7321.19 | MFN import duty | 10% | |

| EAC, COMESA | Cooking appliances and plate warmers, including for solid fuels | HS 7321.19 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Cooking appliances and plate warmers, including for solid fuels | HS 7321.19 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Cooking appliances and plate warmers, including for solid fuels | HS 7321.19 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Other appliances — for gas or gas+ | HS 7321.81 | VAT | 25% | |

| EAC, COMESA | Other appliances — for gas or gas+ | HS 7321.81 | Other taxes and tariffs | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Other appliances — for gas or gas+ | HS 7321.81 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Other appliances — for gas or gas+ | HS 7321.81 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Other appliances — for liquid fuels | HS 7321.82 | MFN import duty | 25% | |

| EAC, COMESA | Other appliances — for liquid fuels | HS 7321.82 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Other appliances — for liquid fuels | HS 7321.82 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Other appliances — for liquid fuels | HS 7321.82 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Other appliances — for solid fuels | HS 7321.89 | MFN import duty | 10% | |

| EAC, COMESA | Other appliances — for solid fuels | HS 7321.89 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Other appliances — for solid fuels | HS 7321.89 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Other appliances — for solid fuels | HS 7321.89 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Parts for cooking appliances and plate warmers | HS 7321.90 | MFN import duty | 10% | |

| EAC, COMESA | Parts for cooking appliances and plate warmers | HS 7321.90 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Parts for cooking appliances and plate warmers | HS 7321.90 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Parts for cooking appliances and plate warmers | HS 7321.90 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Microwave ovens | HS 8516.50 | MFN import duty | 10% | |

| EAC, COMESA | Microwave ovens | HS 8516.50 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Microwave ovens | HS 8516.50 | Other taxes and tariffs | 25% | Excise duty is levied at a rate of 25% of the duty paid value for used domestic appliances, electric fence, air conditiong machines, electric radiators and electric appliances. |

| EAC, COMESA | Microwave ovens | HS 8516.50 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Microwave ovens | HS 8516.50 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

| EAC, COMESA | Other ovens; cooking stoves, ranges, cooking plates, boiling rings, grillers and roasters | HS 8516.60 | MFN import duty | 10% | |

| EAC, COMESA | Other ovens; cooking stoves, ranges, cooking plates, boiling rings, grillers and roasters | HS 8516.60 | VAT | 18% | Value added tax is levied at a rate of 18% of the duty paid value. |

| EAC, COMESA | Other ovens; cooking stoves, ranges, cooking plates, boiling rings, grillers and roasters | HS 8516.60 | Other taxes and tariffs | 25% | Excise duty is levied at a rate of 25% of the duty paid value for used domestic appliances, electric fence, air conditiong machines, electric radiators and electric appliances. |

| EAC, COMESA | Other ovens; cooking stoves, ranges, cooking plates, boiling rings, grillers and roasters | HS 8516.60 | Other taxes and tariffs | 0.6% | Customs processing fee is levied at a rate of 0.6% of the FOB value on all imported goods. Raw materials imported for production purposes are exempted. |

| EAC, COMESA | Other ovens; cooking stoves, ranges, cooking plates, boiling rings, grillers and roasters | HS 8516.60 | Other taxes and tariffs | 1.5% | Railways development levy is applied at a rate of 1.5% of the dutiable value. |

DATA SOURCES:

| Data Source | Link to Source |

| Tanzania Tariff Book | Tariff_CET_2022_Version_25072022_1.pdf |

| TZ Commercial guide | Tanzania – Import Tariffs |

| TZ Exempts summary | VAT Act 2014 – Whats exempt? Whats not? | S R AUDITORS |

| Other taxes & duties | Tanzania Trade Portal |

Carbon

Tanzania has 23 registered cookstove projects. These projects have generated 1.4 million carbon credits to date.

Click ‘Read more’ to explore more.

- Total Credits Issued: 1,446,926

- Total Credits Retired: 285,397

- Number of Projects: 23 (18 GS + 5 VCS)

- Count of Project Developers: 12

Source: Voluntary Registry Offsets Database (Berkeley Carbon Trading Project)

Results Based Finance

Click ‘Read more’ to explore the table of Results Based Finance projects

| Name | Lead | Status | Dates | Applicable Fuels | Fund size for clean cooking | Total fund size |

| CookFund Programme | United Nations Capital Development Fund (UNCDF) | Completed | 2021-2024 | LPG, Biomass stoves | €1.3m | €17m |

| Rural Energy Agency(REA) Subsidy | Rural Energy Agency (REA) | Active | Improved cookstoves, electric cooking | Not disclosed | $4m | |

| Tanzania Clean Cooking Project (TCCP) | Africa Enterprise Challenge Fund (AECF) | Active | 3 Years | $3.75 | $3.75 | |

| Modern Cooking Facility for Africa | Nefco (Nordic Environment Finance Corporation) | Active | Ethanol, Electric Cooking | €16m | €16m |

Connect With Us

If you’d like to see more data on this page, please email carbon@cleancooking.org or fill in the form below.